Krishnan Srinivasan was 35 when he walked into his manager's cabin and resigned. He didn’t resign because he had another job lined up or because he was burned out. He resigned simply because he no longer needed to work.

For the last nine years, the Bengaluru-based software engineer had lived on 40 per cent of his salary, invested the rest with surgical discipline, and built a corpus large enough to fund the rest of his life. He was, by any conventional measure, young enough to be mid-career. He chose to be done. Krishnan is not a lottery winner or an heir. He is a practitioner of FIRE—and he is far from alone.

What is FIRE, and Where Did It Come From?

FIRE stands for Financial Independence, Retire Early. At its core, it is a personal finance philosophy built around one radical idea: that retirement is not an age but a number.

The modern FIRE movement traces its intellectual roots to the book, “Your Money or Your Life” by Vicki Robin and Joe Dominguez, which argued that you are trading your “life energy” for money. In simple terms, the time you worked to earn money. The book, however, asked whether the trade was worth it.

The concept gained mainstream velocity in 1998 when financial researcher William Bengen established the "4% rule": A retiree can withdraw 4 per cent of their invested corpus annually with a high probability that the money will outlast them over a 30-year horizon.

From these two ideas emerged a formula that FIRE adherents now treat almost as gospel.

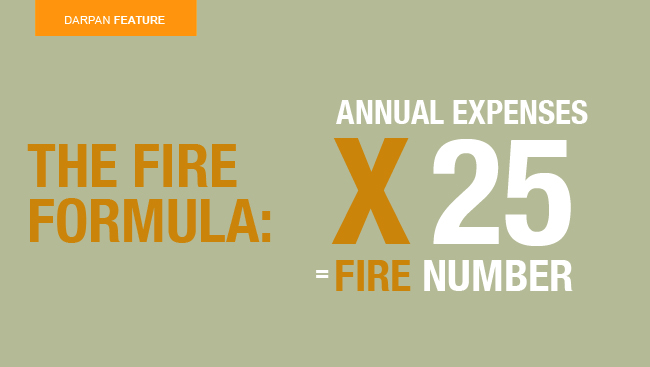

To calculate your FIRE number, you estimate your annual expenses, then multiply by 25. If you spend CAD 50,000 a year, your FIRE number is CAD 1,250,000. That is the corpus you must accumulate, by investing in equities or mutual funds, before you can stop working and live off returns.

The aggressive among them target a savings rate of 50 to 70 per cent of income. The extreme fringe pushes it to 80 per cent. Within the movement, variations have emerged to match different ambitions.

LeanFIRE targets a minimalist lifestyle with a smaller corpus.

FatFIRE targets early retirement without giving up comfort.

BaristaFIRE involves reaching partial financial independence and supplementing with light, low-stress work, the financial equivalent of coasting.

Why are Millennials Increasingly Obsessed with FIRE

No generation has taken to FIRE quite like Millennials, and the reasons are not hard to find. This is a cohort that entered the workforce during or just after the 2008 financial crisis. Millennials—born between 1981 and 1996—watched their parents lose jobs, savings, or both, and internalized a deep skepticism of the employee-employer relationship.

The pandemic sharpened that skepticism further. Mass layoffs, the sudden proof that remote work was always possible, and the jarring experience of watching life shrink to a screen all prompted a reckoning with the question FIRE has always asked: Is this how I want to spend my finite time?

Social media has turbocharged the movement's spread. Reddit forums like r/financialindependence have millions of members sharing savings milestones, portfolio strategies, and resignation letters.

Back home in Canada, FIRE has its own twist amid the rising cost-of-living crisis. Here, Index fund investing is the dominant vehicle to achieve the FIRE figure because no single company’s collapse can wipe out the portfolio.

Interestingly, Canada's universal healthcare system gives FIRE aspirants a structural leg up over their American counterparts. Since coverage is not tied to employment, Canadians who retire early don't face the potentially crippling insurance costs that Americans must budget for a FIRE lifestyle.

There is also generational math at play. Millennials who entered high-paying tech or finance roles in their twenties discovered, sometimes by accident, that high income combined with controlled lifestyle inflation could compound into independence faster than anyone told them was possible.

The Pitfalls Nobody Posts About

For all its appeal, FIRE has serious fault lines. The 4 per cent rule was derived from US market data over a specific historical period. Hence, its applicability to Indian or Canadian markets, with their own inflation dynamics and market volatility, has remained a matter of active debate. Moreover, assuming a 6 to 7 per cent real return on equity over decades involves optimism that markets may not always honor.

There is also the underestimated threat of lifestyle inflation post-retirement. For example: children's education, medical emergencies, and/or aging parents. Healthcare costs alone can devastate a corpus that looks comfortable on a spreadsheet.

Then there is the psychological dimension that FIRE literature often glosses over. Identity, structure, social belonging: For many people, work provides all three. Early retirees frequently report unexpected aimlessness, a condition some researchers have started calling ‘purpose poverty’. A surprising number return to work, not for money, but for meaning.

The Bottom Line

FIRE is not a universal blueprint. It is a framework for asking harder questions about time, money, and what you are trading one for the other. Its most valuable contribution is not the retirement math but the insistence that financial decisions be made consciously rather than by default. Whether you retire at 40 or 65, the discipline to live below your means and invest the difference is counsel that ages well. The dream of never working again may be the headline, but financial intentionality is the actual story.